The Japanese economy unexpectedly stalled in a technical recession in the fourth quarter of last year, and the market’s confidence in the Bank of Japan’s interest rate hike was shaken. The probability of raising interest rates before April once dropped rapidly from 73% to about 63%.

In a recent report, UBS economists Go Kurihara and Masamichi Adachi pointed out that the current economic weakness in Japan may be seen by the outside world as a driving force preventing the Bank of Japan from opening the normalization of monetary policy, butAs long as the Bank of Japan can effectively prove that consumer spending will start to increase, they have reason to adjust monetary policy.Therefore, April is the window for the Bank of Japan to raise interest rates by 10 basis points, when the benchmark interest rate will be raised to 0.

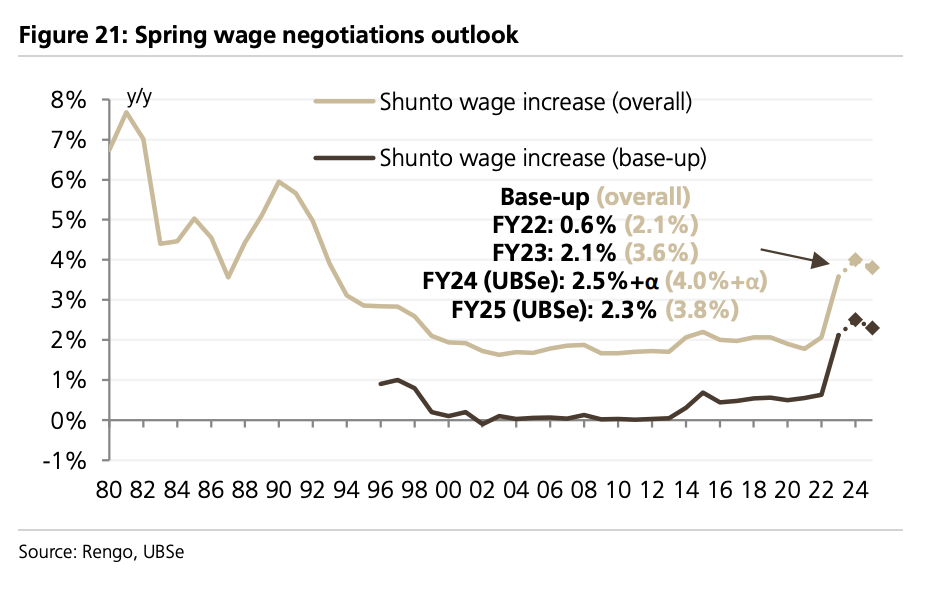

UBS believes that CPI will slow down until the end of 2024, which will reduce the impact on real wages. The real wages of Japanese residents are expected to accelerate in 2024, which will promote consumer spending and economic growth.

Considering Japan’s economic trend in 2024 and the future, UBS changed its policy path expectations for the Bank of Japan after April.It is expected that the Bank of Japan will not further adjust interest rates this year after April.(Previously, it was expected to raise interest rates by 25 basis points again in July to raise interest rates to 0.25%).There will be three interest rate hikes of 25 basis points in 2025, and the policy interest rate will reach 0.75% by the end of 2025.

UBS believes that if the US economy is not in recession, it is still possible for the Bank of Japan to raise interest rates by 25 basis points in October this year, so that the policy interest rate will reach 0.25% by the end of 2024.

On February 15, local time, the Cabinet Office of Japan announced preliminary statistics showing that in 2023, Japan’s real GDP increased by 1.9% year-on-year, and its nominal GDP increased by 5.7%, which was about 4.2 trillion US dollars. The nominal GDP in US dollars was surpassed by German GDP.Japan fell from the third largest economy to the fourth largest economy.

On a quarterly basis, Japan’s GDP growth rate contracted by 0.4% in the fourth quarter of 2023 after contracting by 3.3% in the third quarter of 2023.Unexpectedly fell into a technical recession.

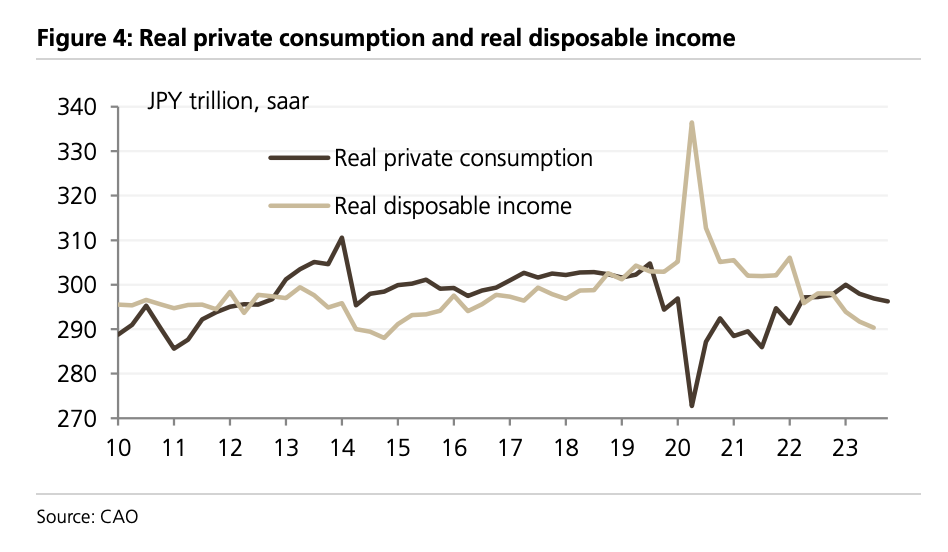

UBS pointed out that the weak consumption of Japanese residents has become an important reason for the technical recession, and it has always been a long-term concern of the government. In the fourth quarter, the consumption season of Japanese residents contracted by 0.9% year-on-year, which dragged down GDP by 0.5 percentage points, and it shrank for the third consecutive quarter. There are three factors: 1. The real wage income of residents continued to decline, 2. Enterprises did not increase capital expenditure as scheduled, and 3. Government public expenditure increased:

1. From the perspective of wage growth, Japan’s wage growth still failed to catch up with the price increase. In the fourth quarter, Japan’s real wages fell by 1.9% year-on-year, which led to a decline in actual expenditure.

It is worth mentioning that the weak actual consumption also reflects the problem of Japan’s population decline. At present, Japan’s population is decreasing by 0.5% every year. In 2023, the consumption of inbound tourists became a major pillar of the economy, but compared with the consumption of Japanese nationals, the consumption of tourists only accounted for 1.5%.

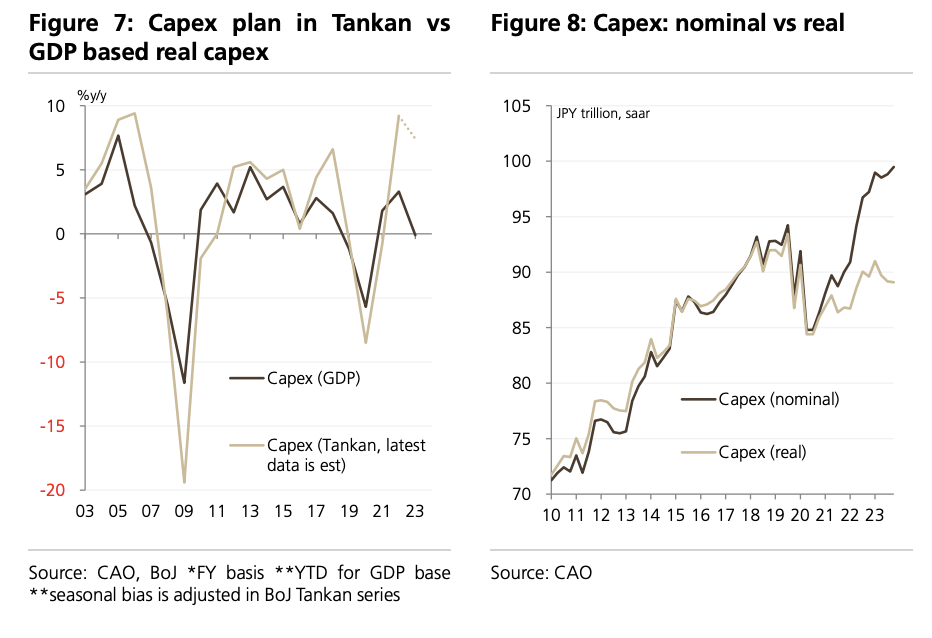

2. Although the business survey shows that enterprises plan to increase capital expenditure (that is, enterprises plan to invest in new equipment, technology or buildings to expand or enhance their productivity), in fact, they have not seen the recovery of capital expenditure in the past year, which on the one hand reflects the difference between name and reality, and on the other hand, it may be because of supply constraints that equipment installation and building structure are delayed.

In addition, supply constraints are also one of the reasons for the stagnant capital expenditure of Japanese enterprises.

Another reason for the weakening of consumption is that the annual growth rate of government expenditure has unexpectedly dropped to -0.9%.In terms of sub-items, the growth of government consumption (-0.5%) and public sector investment (-2.8%) are lower than GDP, which shows that fiscal policy is in a marginal tightening state in the fourth quarter.

UBS predicts that Japan’s real GDP growth in 2024 will be 0.1% lower than that in 2023, falling to 1.0%.The driving force of economic growth has shifted from external demand (including the consumption of inbound tourists) to domestic demand. With the acceleration of wage growth and the slowdown of CPI, the real wages of Japanese residents will increase.:

On the one hand, the decline in household consumption has narrowed month-on-month, and imported inflation such as energy has dropped, which will alleviate the impact on real wages; At the same time, Japan’s labor shortage is becoming more and more serious. The strategy of increasing labor supply by increasing the labor participation rate of women and the elderly has reached a bottleneck, and the government is also calling on employers to raise wages, which increases the possibility of wage increase in Japan, and a virtuous circle of wages and prices is expected to be established.

UBS believes that by the end of 2024, the deflation of core CPI will stop, and the prices of other goods and services except food and energy will no longer continue to fall, mainly because inflation expectations are rising and there is no downward pressure on output:

According to our latest forecast, by the end of 2024 and 2025, Japan’s core CPI will be 1.6% and 1.7% respectively.It is 0.1 percentage points lower than the previous forecast..

We predict that wage growth in Japan will accelerate significantly in 2024. However, the slowdown in CPI in 2024 and the decline in corporate profits will not continue until 2025. We believe that the wage growth rate will slow down in 2025.

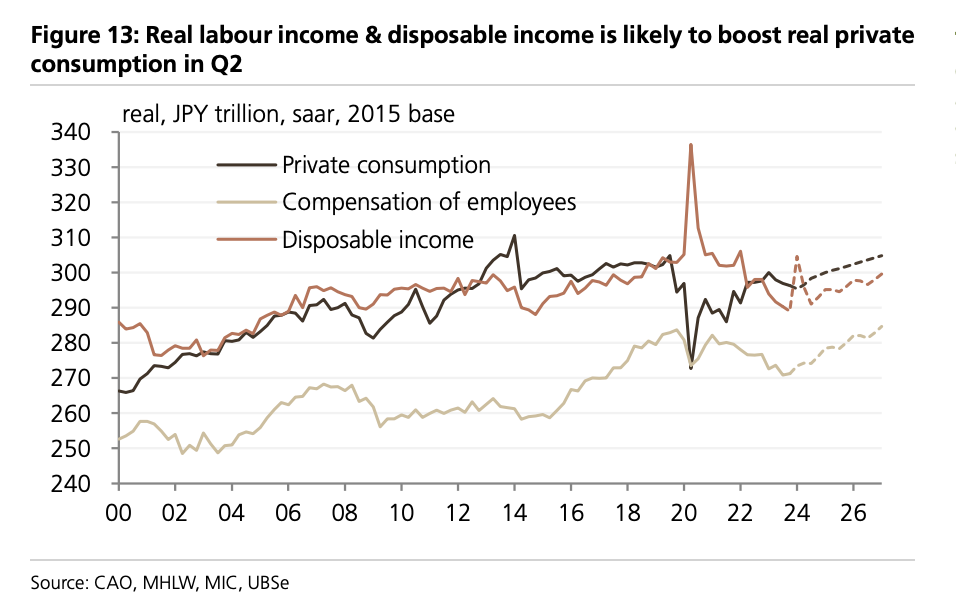

Due to the increase in real wages, we expect that the real disposable income of Japanese residents will also increase. At the same time, in June this year, a one-time tax reduction and cash payment will promote actual consumption.

According to the latest data, although Japan’s CPI in January was higher than expected, the slowdown trend did not change. In January, the overall CPI rose by 2.2% year-on-year, which continued to slow down from the previous value of 2.6%. In January, the core CPI (except fresh food and energy) in the core rose by 3.5% year-on-year, which was 3.7% lower than the previous value.

UBS said that their forecasts for Japan’s GDP and CPI were set in the second and third quarters of this year when the GDP of the United States shrank and there was a technical recession. If there is no recession in the United States, under such a narrative, Japan’s inflation level will be higher than that of the long-term depreciation of the yen.

Considering the above factors, UBS concluded that if the external environment is stable, that is, there is no serious recession in the United States, Japan’s inflation expectations will rise, which means that the Bank of Japan has reason to start a normalized monetary policy.

Therefore, UBS believes that the Bank of Japan will still adjust the benchmark interest rate to 0 after April 2024, but it will not raise interest rates for the rest of this year (it was expected to raise interest rates by 25 basis points in July), but it still judges that the Bank of Japan will raise interest rates three times in 2025, each time by 25 basis points.

This article is from Wall Street. Welcome to download the APP to see more.